If you’ve recently been informed about a past tax debt, you might be wondering whether it ever goes away. The good news is that it can. Federal law gives the IRS a fixed legal window to collect what you owe, and once that window closes, the debt expires.

Your actions matter, though, because you could restart the clock or impact the collection timeline in other ways. The clock also doesn’t start until the date your tax is assessed, so the IRS’s actions matter, too.

Here’s what you need to know about how this deadline works and what it could mean for your tax balance.

Does IRS Tax Debt Expire After 10 Years?

Yes. The IRS doesn’t get to chase that debt forever. Once a tax is assessed, they have 10 years to collect it, and that deadline has a name: the Collection Statute Expiration Date (CSED). When the CSED hits, their legal right to collect is gone.

The balance doesn’t get passed to another agency or sit there indefinitely. It’s done.

So what actually happens when that date arrives? Here’s the direct answer:

- The debt becomes legally uncollectible

- The IRS must stop all active collection efforts tied to that assessment

- Any tax liens associated with the debt become unenforceable

- You’re no longer legally obligated to pay, even if the original balance was significant

One important detail: the 10-year clock doesn’t start from the date a return was due or the date you filed. It begins on the date the tax was assessed, which is typically close to the filing date if you submitted a return with a balance owed.

If the IRS never received a return from you, they may file a Substitute for Return on your behalf, and the CSED begins from that assessment date instead. If you later file your own return, the CSED does not reset. If you’re dealing with unfiled tax returns, resolving those is often the first step toward getting the collection clock started and knowing exactly where you stand.

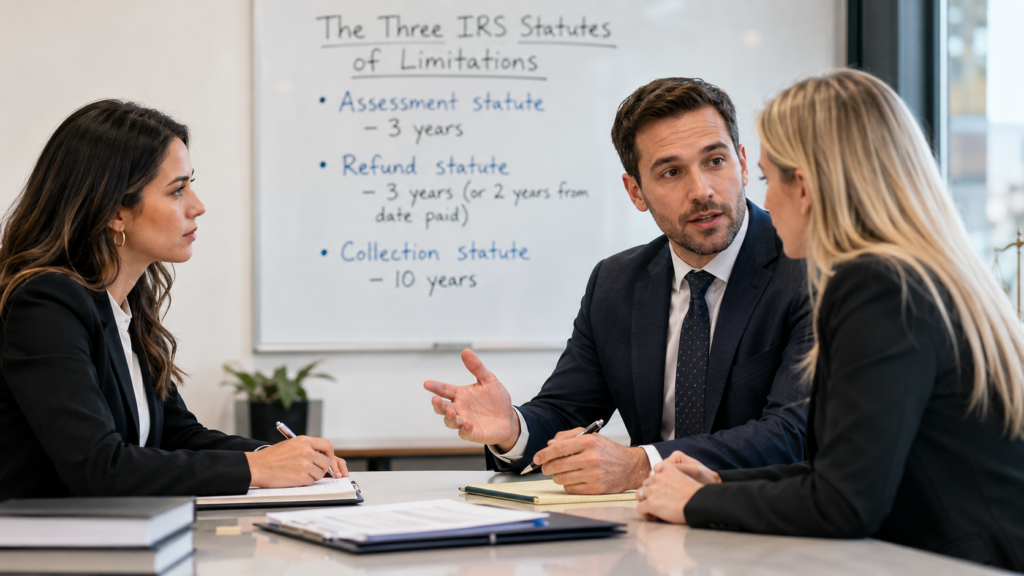

The Three IRS Statutes of Limitations You Should Know

Most people only hear about the 10 year collection rule. But the IRS actually operates under three separate statutes of limitations, each covering a different stage of the tax process. Knowing all three matters because they all affect your legal standing with the IRS.

- Assessment statute: The IRS generally has three years after a tax return is due to assess a tax debt. Once that window closes, they can’t add a new tax bill for that year.

- Refund statute: The IRS will only honor a tax refund, credit, or claim within three years from the date you filed your return, or two years from the date you paid, whichever is later. Miss that window, and you forfeit the refund.

- Collection statute: Once a tax is assessed, the IRS has 10 years to collect it. This is the CSED, and it’s the one most taxpayers with back tax debt need to track closely.

One more thing worth knowing: the CSED is tied to each individual tax assessment. If you owe for multiple tax years, or if you have separate penalty assessments on top of the original debt, each of those carries its own CSED. You could have several expiration dates on your account at the same time, each on a different timeline.

The CSED Waiver: What to Do If the IRS Asks You to Sign

There’s one scenario the IRS doesn’t advertise. If you’re entering into a Partial Payment Installment Agreement (PPIA) and the repayment term would stretch beyond your current CSED, the IRS may ask you to sign Form 900, a Tax Collection Waiver. Signing it extends your CSED, giving the IRS more time to collect beyond the standard 10-year period.

You are not legally required to sign it. The IRS is limited to requesting a waiver of no more than five years on a PPIA. Before you agree to anything that touches your CSED, get a qualified tax professional involved.

What Can Pause or Extend Your Collection Timeline

Here’s something a lot of taxpayers don’t realize: that 10-year clock can be paused. When it is, the CSED gets pushed further out by however long the pause lasted. This is called tolling, and it can quietly add months or even years onto your collection timeline without you knowing.

Once whatever triggered the pause is resolved, the clock picks back up right where it left off.

A few events can extend the clock on your tax debt:

- A bankruptcy filing pauses the clock

- The clock is paused while the IRS reviews an Offer in Compromise request; if the OIC is rejected, the CSED stays suspended for an additional 30 days after the rejection

- The timer stops temporarily if you request a Collection Due Process (CDP) hearing

- Collections pause while you are living outside the U.S. or serving in a combat zone

This is one of the most important things to understand about the statute of limitations on tax debt collection. If any of these events occurred during your collection period, your actual CSED could be well beyond the 10-year anniversary of your assessment date.

Estimating your CSED on your own can lead to costly mistakes. You need to verify the actual expiration date directly from your tax transcript.

How to Find Your Collection Statute Expiration Date

Every tax debt has a collection statute expiration date assigned to it. This date is determined based on when the debt was assessed by the IRS, and knowing it precisely is critical. After that CSED date passes, the IRS no longer has a legal right to pursue collection efforts against you.

Here’s how to find and verify your CSED:

- Online IRS account: Log in to irs.gov, head to your tax records, and pull your transcripts from there. It’s the fastest option.

- Form 4506-T: Fill this out and mail it in to request a paper transcript. Give it 5 to 10 business days to arrive.

- Phone: Not a fan of online accounts? Call 800-908-9946, and they’ll mail a transcript to you directly.

Once you have your transcript, go to the transactions section and find the 3-digit IRS transaction code that has a date below it. That date is your CSED. If you have multiple tax years with unpaid balances, review each one separately, since each assessment carries its own expiration date.

Your Options When You Can’t Pay Before the Debt Expires

When you have unpaid back taxes that you genuinely can’t pay off in full, even over time, there are still options available to you. The most common solutions are a partial payment installment agreement and a currently not collectible status. If you also have unfiled returns tied to the debt, addressing those alongside a resolution plan is often the right move.

Partial Payment Installment Agreement (PPIA)

A partial payment installment agreement allows you to make small payments over time until the CSED arrives. Once the CSED passes, the remaining balance will no longer be collectible by the IRS.

Both sides benefit from this arrangement. You won’t have to pay your full tax liability, but the IRS will still recover some of what they’re owed. It’s a practical middle ground when you have some ability to pay but can’t cover the full amount.

Currently Not Collectible (CNC) Status

If you’re genuinely unable to make any payments, you can apply for currently not collectible status. This financial hardship status pauses all collection activity, and you won’t have to make any payments during the pause.

What makes the CNC status particularly useful is that the statute of limitations clock continues to run the entire time you’re in this status. The IRS may check on your financial situation from time to time to see if your circumstances have improved, but if they stay the same, you won’t have to pay anything until the CSED passes and the IRS tax debt expires.

Why Simply Waiting Out the Clock Can Backfire

Once you realize the IRS only has ten years to collect on a tax debt, it might be tempting to simply wait it out. While that may make sense if your debt is close to expiring, it’s not always the right call, especially if you have significant assets or a steady income through a traditional employer.

During the collection process, the IRS retains full authority to:

- Pursue wage garnishment directly from your employer

- File a levy against your property, including bank accounts

- Confiscate and sell your property to satisfy the remainder of your debt

On top of that, penalties and interest continue accumulating while you wait, which can significantly increase the total balance. Rather than risk your professional reputation, physical property, and overall quality of life, it’s wise to consult with a tax resolution specialist to weigh your options and determine the best strategy based on your actual CSED.

Know Where You Stand Before the Clock Runs Out

Once the Collection Statute Expiration Date passes, the IRS loses its legal right to collect, and that debt is no longer enforceable. But the path there isn’t always straight. Tolling events can push your CSED further out than expected, and waiting without a plan can leave your wages, bank accounts, and property exposed.

The tax attorneys at W Tax Group work with taxpayers nationwide to calculate CSEDs, identify the right resolution strategy, and handle the IRS process from start to finish. There’s almost always a path forward. Contact us today for a free consultation.

Frequently Asked Questions

Can the IRS collect after 10 years?

Generally, no. Once the CSED passes, the IRS can’t legally come after that debt anymore. That said, if something paused the clock during the collection period, like a bankruptcy filing, an Offer in Compromise review, or time spent living abroad, your CSED may stretch well past 10 years. The calendar date isn’t always the whole story.

What happens after 10 years of owing the IRS?

Assuming no tolling events pushed the CSED out, the debt expires, and the IRS has to stop collecting. Any levies or wage garnishments tied to that debt can’t be enforced anymore. It doesn’t get handed off to a collections agency either. It’s simply gone.

Why is the IRS trying to collect after 10 years?

Most likely because your CSED isn’t where you think it is. Certain events pause the collection clock, and a lot of taxpayers don’t realize it happened. Bankruptcy, an Offer in Compromise, a CDP hearing request, living abroad – any of these can push the CSED well past that 10-year mark. Pull your transcript and check the actual date before assuming the IRS is out of bounds.

Does the IRS forgive tax debt after 10 years?

Not technically. The IRS doesn’t call it forgiveness. What actually happens is that the debt becomes unenforceable once the CSED passes. They can still take your money if you voluntarily send it, but they can’t make you. No demands, no levies, no garnishments. Practically speaking, that’s about as close to forgiven as it gets.