IRS Substitute for Return (SFR): What Happens When the IRS Files For You

You missed the filing deadline. It feels fine at first. Life got busy, you’ll deal with it later, and suddenly it’s been months.

Here’s what most people don’t know: the IRS isn’t sitting around waiting for you. At some point, they stop asking and just file a return for you, and it’s almost never in your favor.

That return is called a Substitute for Return, and the tax bill it generates is almost always far larger than what you’d actually owe.

Here we break down what gives the IRS the right to do this, how the notice process plays out, how the SFR gets calculated, what it’ll cost you, and what you can actually do about it.

Substitute for Return (SFR): The Legal Authority Behind It

An SFR is a return the agency builds from whatever income data third parties have already reported (W-2s, 1099s, K-1s) when you haven’t filed your own.

The authority to do this comes from Internal Revenue Code Section 6020(b)(1), which lets the IRS pull together a return from its own records and anything else it can get its hands on. It kicks in when you haven’t filed, or when what you did file was false or fraudulent.

Under Internal Revenue Manual Section 4.25.8.5(2), the IRS can prepare and file a substitute tax return on your behalf when two specific conditions are met:

- The tax return filing due date and the extension date have both passed.

- Every attempt the IRS made to get you to file went nowhere.

Once those boxes are checked, the IRS moves. It assesses what it thinks you owe and starts collection. The agency pulls W-2s, 1099s, and K-1s from employers, clients, and financial institutions to piece the return together.

Got a delinquent, unfiled tax return and IRS notices piling up? The clock is already running. They won’t hold off forever.

IRS Warning Notices Before a Substitute Return Is Filed

The IRS doesn’t file an SFR without warning. Before it starts, the agency sends a sequence of escalating IRS notices designed to give you every opportunity to file on your own.

You’ll typically receive the first notice around ten months after the return due date or extension date, or sooner if the IRS detects a filing obligation on your account with no return on record.

The notice sequence runs as follows:

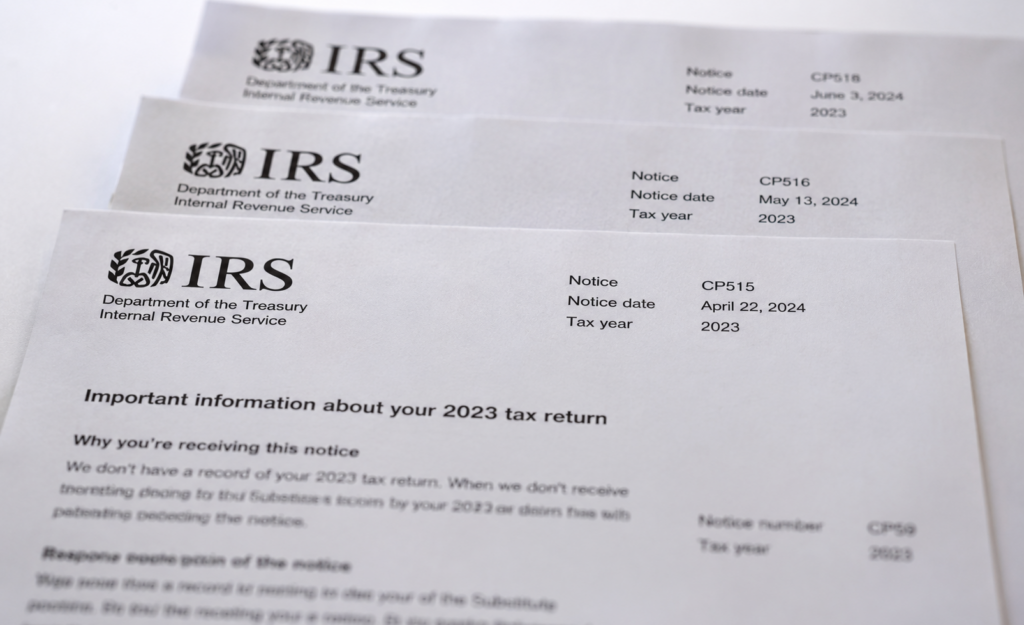

- Notice CP59, the initial notice, informs you that the IRS has no record of your tax return for the prior year.

- Notice CP515, a reminder, tells you the IRS still has no record of your return on file.

- Notice CP516, a more urgent reminder, signals the IRS intends to escalate its efforts to get you to file.

- Notice CP518, the final notice, warns you the IRS is about to take further action, including filing a substitute return on your behalf.

If you don’t file a return or respond to any of these notices, the IRS proceeds to prepare the SFR. Each notice is one step closer to assessment and collection. Respond to any one of them by filing your return, and you stop the process entirely.

How the IRS Calculates Your Tax Liability on an SFR

This is the section that matters most financially. The IRS doesn’t try to calculate your accurate tax liability when it prepares an SFR. It constructs a bare-bones assessment built to trigger collection, using only what third parties reported.

The Filing Status Problem

The IRS defaults to the least favorable filing status when preparing an SFR, typically Single or Married Filing Separately. If you’re married and would qualify for Married Filing Jointly, which carries lower tax rates and higher income thresholds, that benefit is not applied.

If you qualify as Head of Household, that’s also ignored. The result is a higher tax bracket, a smaller standard deduction, and a larger bill.

No Business Expenses, No Credits, No Itemized Deductions

The ASFR system applies the standard deduction but stops there. It does not apply itemized deductions, business expenses, or credits. Specifically, the IRS won’t apply:

- Business expenses against 1099 income

- Mortgage interest your bank already reported on Form 1098

- Above-the-line deductions like student loan interest and retirement contributions

- Credits like the Earned Income Tax Credit, the Child Tax Credit, or the education credits

For self-employed workers and contractors, the gap between what the SFR says you owe and what you’d actually owe can be dramatic. Here’s a real-world scenario: Taxpayer A is a contractor bringing in $350,000 gross, all on 1099s.

His actual expenses, covering equipment, materials, wages, office costs, marketing, licenses, and depreciation, add up to $270,000. Real taxable income: $80,000.

He doesn’t file. The IRS files an SFR on the full $350,000. That is not a rounding error.

$270,000 in legitimate deductions, gone. It happens all the time to self-employed taxpayers who don’t file. If that’s your situation, our unfiled tax return help team can step in before the assessment gets locked in.

The SFR Filing Steps: Letter 2566 to Final Assessment

Once the IRS’s Automated Substitute for Return (ASFR) Program finishes preparing the SFR, the formal notice and assessment process begins. This section covers what that looks like in sequence.

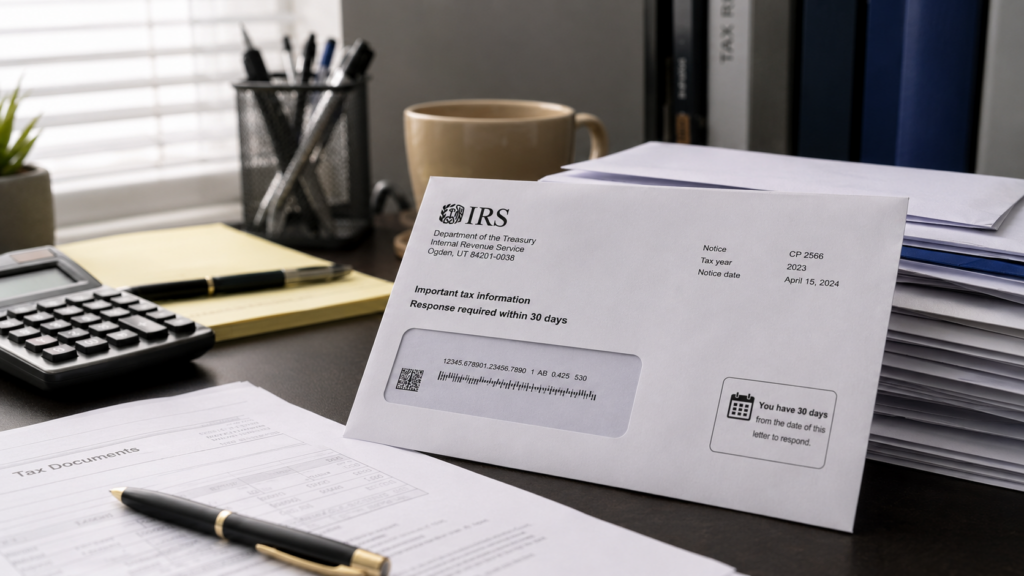

Letter 2566: Your 30-Day Window

The ASFR system automatically generates Letter 2566 and sends it to you. This letter informs you that:

- No tax return is on file for the specified tax year.

- The IRS has prepared a Substitute for Return on your behalf.

- Tax, penalties, and interest were calculated based on the income third parties reported.

- Filing an original return for the year will likely be to your advantage.

You have 30 days from this letter to take one of the following actions:

- File the original return for the specified year.

- Submit a written statement explaining why filing a return isn’t necessary.

- Provide additional information you want the IRS to consider.

- Appeal the proposed IRS assessment.

Taxpayers who agree with the assessment can complete and submit a Consent to Assessment and Collection form. Agreeing without professional review is rarely advisable, since the SFR assessment is almost always overstated.

Letter 3219N: The 90-Day Statutory Notice of Deficiency

If you don’t respond to the 30-day letter, the IRS sends a 90-day letter via registered mail. In most cases, this is Letter 3219N, a Statutory Notice of Deficiency. It explains exactly how the IRS calculated the tax, penalties, and interest, and lists the contact for the examiner on your case. The letter also notes that you may qualify for a payment agreement once you become tax-compliant.

Your options at this stage are:

- File a Tax Court petition to challenge the proposed assessment within 90 days of the letter’s date.

- File your original return for the year.

- Agree to the assessment by submitting the Response Form included with the letter.

Once this 90-day window closes without a response, the IRS assesses the full proposed tax, penalties, and interest and moves into active collections.

You also lose the right to challenge the liability in Tax Court without first paying the assessed amount. That’s why responding to a notice of deficiency on time is critical.

Manual SFR Cases

Some cases are handled manually by IRS tax examiners rather than the automated system. When that happens, you’ll receive Letter 1862 as the 30-day notice and Letter 3219 as the 90-day letter. After assessment, IRS Notice CP22E confirms your tax liability.

What an SFR Filing Actually Costs You

An SFR doesn’t just leave you with an inflated tax bill. It sets off a chain of financial and legal consequences that compound the longer the matter goes unresolved.

Immediate Financial Damage

In addition to a higher-than-necessary tax liability, you’re facing:

- Failure-to-file penalty: Typically 5% of unpaid taxes for each month the return is late, up to a maximum of 25%. The IRS applies this retroactively to the original return due date. See how failure-to-file penalties are calculated.

- Accruing interest: Interest runs on any unpaid taxes from the original due date until you pay. The rate adjusts quarterly and equals the federal short-term rate plus 3%.

Impact on Your Legal Rights and Future Options

Beyond the financial hit, an SFR filing affects your legal rights in ways that aren’t always obvious:

- Loss of refunds: If you’re entitled to a refund, you must file within three years of the original due date to claim it. An SFR filed after that window could mean losing that refund permanently.

- Future filing obligation: An SFR does not eliminate your requirement to file a proper return for that year. Filing your own return replaces the SFR and typically results in a more accurate, lower assessment.

- IRS collection actions: An unpaid SFR assessment can trigger IRS levies on wages or bank accounts. They can also drop a tax lien on your property, which kills your credit and makes selling or refinancing a nightmare.

- First-time penalty abatement: Wait until the IRS has already reached out before filing, and first-time penalty abatement is likely off the table.

- CSED clock delay: The IRS has 10 years to collect under the collection statute of limitations. The SFR itself does not start that clock. The assessment does. Once the IRS assesses the tax (typically after the 90-day notice period expires), the 10-year collection window begins under IRC 6502. Until then, there’s no deadline for the IRS to collect.

Bankruptcy and State Tax Risks

Two consequences that most taxpayers don’t think about until it’s too late:

Bankruptcy discharge. If you ever need to discharge tax debt through bankruptcy, SFR-assessed liabilities create a serious complication. Under the Bankruptcy Code, the IRS-filed SFR under IRC 6020(b) does not satisfy the filing requirement needed to make tax debt eligible for discharge.

In many jurisdictions, that means the SFR-assessed tax debt cannot be discharged even if the debt is years old. Filing your own return first, before the IRS files an SFR, keeps your bankruptcy options open.

State tax consequences. The IRS shares federal tax data with state tax agencies. When the IRS creates an SFR, that income information gets sent to the taxpayer’s state.

The state may then assess higher state tax bills or pursue unfiled state returns it didn’t previously know about, creating a second layer of liability on top of the federal assessment.

Don’t lose hope. Even after the IRS has filed an SFR and assessed a tax, you can still act to reduce your liability and resolve the debt.

How To Respond to an SFR and Prevent the Next One

You have options, and acting quickly keeps all of them open.

Your Best Move: File an Original Return

In most cases, filing an original return is the best response to an SFR. Doing so replaces the income-only calculation the IRS used with your actual figures, deductions, credits, and correct filing status.

It almost always results in a significantly lower tax liability.

Before you file, pull your IRS account transcripts to review the exact income and wage information the IRS has on record. Then gather documentation for every deductible item that applies:

- Business expenses and operating costs

- Medical and childcare expenses

- Property tax payments and charitable donations

- Retirement contributions and above-the-line adjustments

File it, and your numbers replace the IRS’s numbers. The SFR is effectively overridden.

Already past the final assessment? You’ll probably need to request an audit reconsideration along with the return. It’s an extra step, but a tax professional can walk you through it.

The Offer in Compromise Exception

There is one exception worth knowing about. If you think you may qualify to settle your taxes for less through an offer in compromise, you might be able to apply for a settlement on the SFR-assessed amount without filing a return first.

This isn’t the right path for everyone. Our team at The W Tax Group can help you determine whether this option makes sense for your situation.

Preventing an SFR Going Forward

If you have prior-year returns still outstanding, file them as soon as possible. The IRS is significantly more likely to initiate SFRs for taxpayers with multiple unfiled years.

In practice, the IRS typically enforces compliance going back six years, though it can go further if fraud is suspected. Going forward:

- Need more time? File Form 4868 for an extension, but make sure you actually follow through and file before that deadline, too.

- Keep clean, complete records of income, deductions, and credits throughout the year, not just at tax time.

- If you’re not required to file and the IRS contacts you, respond in writing explaining that as soon as possible.

Don’t Let the IRS File Your Return

An SFR is an enforcement tool, not a courtesy. The IRS constructs it to collect revenue, not to calculate your accurate liability.

It applies only the standard deduction, uses the least favorable filing status, ignores all credits and itemized deductions, and moves into active collections the moment the assessment is final. Every month you wait adds penalties and interest to an already overstated bill.

At The W Tax Group, we work with taxpayers nationwide to resolve SFR assessments, replace SFRs with accurate original returns, and pursue resolution options like installment agreements, currently-not-collectible status, and offers in compromise.

If you owe back taxes on an SFR assessment, contact us today for a free consultation.

Frequently Asked Questions

What is a substitute for return?

A substitute for return is a tax return the IRS files on a taxpayer’s behalf when that taxpayer has failed to file one.

The IRS uses only third-party income data, with no deductions, credits, or favorable filing status applied, which typically results in a tax liability that is significantly higher than what the taxpayer actually owes.

Can I stop the IRS from filing an SFR?

Yes. Filing your own return before the IRS completes its SFR process is the most effective way to stop it. Responding to the CP59 through CP518 notice sequence promptly, or proactively filing past-due returns, can halt the SFR process before an assessment is made.

How does the IRS calculate an SFR?

The IRS works from third-party income documents (W-2s, 1099s, K-1s) that have been reported under your Social Security number. It picks the worst filing status for you, usually Single or Married Filing Separately, and skips your deductions, credits, and exemptions entirely.

The number it lands on is almost always higher than what you’d owe if you filed yourself.

Does an SFR include tax deductions?

The IRS applies only the standard deduction when preparing an SFR. It does not apply itemized deductions, business expenses, above-the-line adjustments, or any credits such as the Earned Income Tax Credit or Child Tax Credit. This is the primary reason an SFR almost always produces a higher tax bill than a return the taxpayer would file on their own.

Can I replace an IRS Substitute for Return?

Yes. You can file an original return at any point, even after the IRS has already issued an SFR. The IRS will accept and process the original return, and the figures on it will supersede those in the SFR.

What triggers a Substitute for Return?

A missed filing deadline is the main trigger, and the IRS SFR is used in both individual and business filer cases.

Once the due date and any extension date have passed and the IRS has been unable to get you to file, it can initiate the SFR process. Having multiple years of unfiled returns significantly increases the likelihood the IRS acts.

How long does the IRS take to file an SFR?

The IRS typically sends the first notice (CP59) around ten months after the original return due date.

The full notice sequence, from CP59 through CP518 and into the SFR preparation and 30-day and 90-day letter stages, can span several additional months before the assessment is finalized.